Welcome to Part 2 of this article on long-term care planning (you may catch up on Part 1 here). In this segment, we will discuss the key challenges faced by primary caregivers and explore effective strategies for mitigating financial risks associated with severe disability.

Caregiving is often an emotional and physical journey, filled with challenges that can impact both the caregiver and the person receiving care.

Understanding these challenges and planning ahead can make a significant difference in managing the associated financial burden. From navigating the emotional toll to addressing the financial implications, we will guide you through practical solutions to ensure that you are prepared for the complexities of long-term care.

Challenges (Primary Caregiver)

Being a primary caregiver is not an easy job. It comes with several challenges that can vary based on the specific circumstances and the needs of the person being cared for. Some of the challenges faced by primary caregivers include:

- Emotional Stress

- Emotional Toll: Watching a loved one suffer or decline can be emotionally exhausting.

- Burnout: The constant demands can lead to physical and emotional burnout, with caregivers often feeling overwhelmed.

- Guilt: Caregivers may feel guilty if they feel they are not doing enough or if they experience frustration.

- Physical Demands

- Fatigue: Caregiving can involve physical tasks such as lifting, bathing, and moving the person, leading to exhaustion.

- Health Impact: The physical toll can impact the caregiver’s own health, leading to chronic conditions like back pain.

- Time Constraints

- Loss of Personal Time: Caregiving often consumes a significant amount of time, leaving little time for personal hobbies or relaxation.

- Disruption of Routine: Daily routines can be disrupted, making it difficult to balance caregiving with work or personal responsibilities.

- Financial Burden

- Cost of Care: Caregiving can be expensive, especially if medical care, special equipment, or home modifications are required.

- Loss of Income: Many caregivers reduce work hours or leave their jobs, leading to a decrease in household income.

- Social Isolation

- Reduced Social Life: Caregiving responsibilities often limit social interactions and lead to feelings of isolation.

- Neglect of Relationships: It’s common for caregivers to neglect their own relationships, including friendships and marriages, as they focus on their caregiving duties.

- Lack of Support

- Limited Resources: Many caregivers struggle with a lack of external support, such as respite care, community services, or other family assistance.

- Navigating Systems: Accessing and managing healthcare, legal, or social services can be complex and confusing.

- Mental Health Impact

- Anxiety and Depression: The emotional and physical pressures of caregiving can lead to mental health issues like anxiety and depression.

- Cognitive Overload: Managing medications, appointments, and care schedules can lead to cognitive overload, causing mental fatigue.

- Legal and Ethical Challenges

- Lasting Power of Attorney (LPA): Caregivers may have to make legal decisions on behalf of the person they care for.

- End-of-Life Decisions: Making decisions about life-prolonging treatments or care can be ethically and emotionally difficult.

How Does It Impact Us Financially?

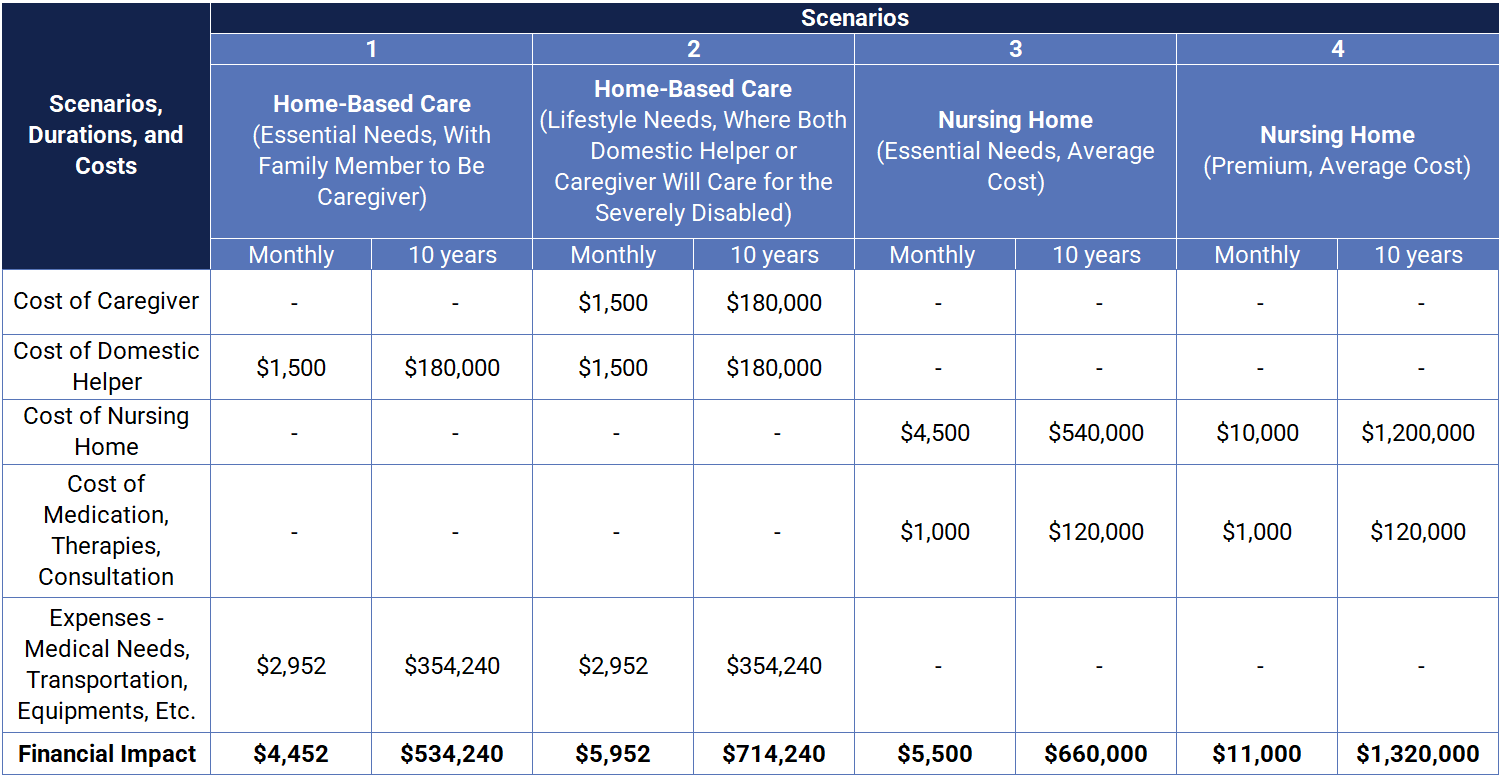

This would depend on the level of care that we are looking for. If the cost of staying in nursing home is $5,000 a month (non-subsidised), and we are severely disabled for the next 10 years, it will cost us approximately $600,000 ($5,000 x 12 months x 10 years). The hard truth is we will not know how long we will be disabled and how financially ready we are when the time comes. It can be five years, 10 years, or even more than 20 years. This depends largely on the nature of the disability and any underlying medical conditions. Here are scenarios showing how much healthcare expenses and opportunity costs could add up if one suffers from severe disability:

Source: By Havend 2024

Based on the scenario of understanding the financial impact, if the disability event extends beyond 20 years, the cost will essentially double.

Inflationary Risk

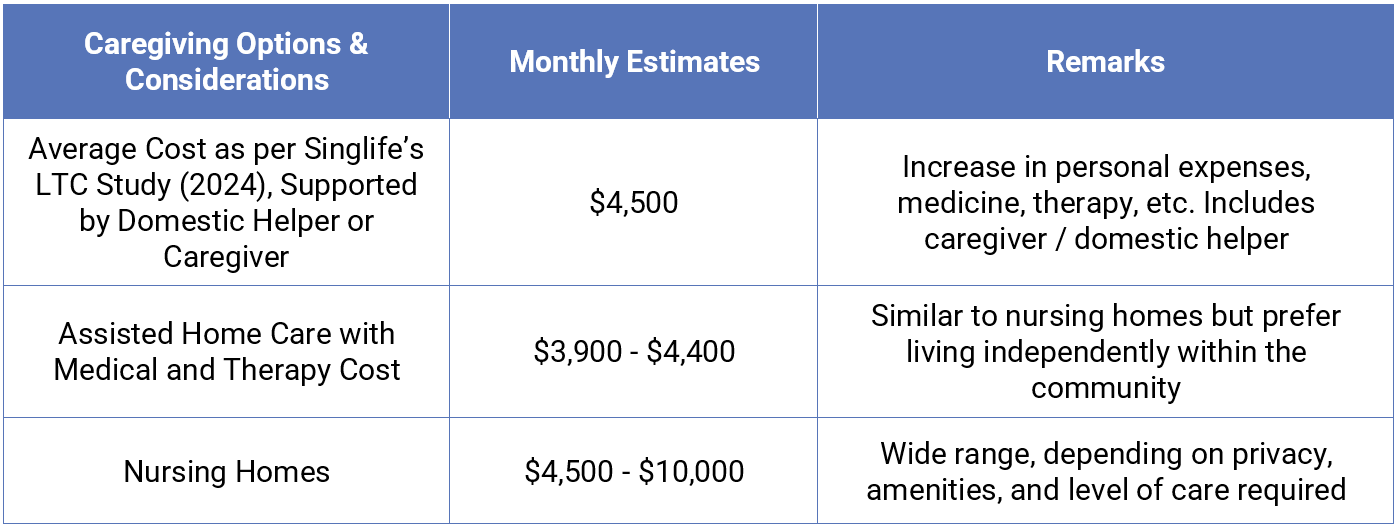

Another factor that will impact us is healthcare inflation. According to the Department of Statistics Singapore, healthcare inflation has increased by 4.5% in the year 2023. Over the past 60 years, healthcare inflation has had a compound average rate of 2.85%. This means the cost of long-term care will continue to rise in the future. If the cost of a nursing home is $4,500 per month (non-subsidised), it could potentially rise to $8,000 per month (non-subsidised) in 10 years based on a 2.85% inflationary rate.

How Do We Mitigate This Area of Risk?

When we are planning to mitigate the financial impact, there are several ways to reduce the financial risks of long-term care.

Here are three types of financing options for long-term care needs:

(1) Government Insurance (ElderShield / CareShield Life)

ElderShield 300 was first introduced in 2002, providing payouts of $300 per month for up to five years upon severe disability. It was later reviewed and revised in 2007 to offer better benefits of $400 per month for up to six years. The benefits we receive depend on the scheme we have joined.

On 1 October 2020, CareShield Life was introduced, offering better benefits than ElderShield for all Singapore Citizens or Permanent Residents born in 1980 or later, or when they turn 30, whichever is later. CareShield Life provides a starting payout of $600 per month from 2020 for a lifetime, with the coverage amount increasing over time.

Another key feature of CareShield Life is that Singaporeans or Permanent Residents born in 1980 or later, with pre-existing medical conditions and/or disabilities, are also covered. Those born in 1979 or earlier can choose to join CareShield Life if they have not developed severe disability.

(2) Personal Insurance (Long-Term Care Supplement)

In addition to government insurance, we can enhance our coverage through personal insurance. Three insurers in Singapore offer long-term care supplements – Singlife, Great Eastern, and Income. The monthly coverage from each insurer is up to $5,000 per month. We can also use up to $600 per year from our Medisave account to pay for the premiums.

(3) Personal Assets

The final option for financing long-term care is through personal assets such as retirement funds (Annuities, CPF, etc.), savings, investments, and even Medisave. Starting from 2020, severely disabled Singapore Residents aged 30 and above can withdraw up to $200 per month for long-term care. The withdrawal amount depends on the Medisave balance at the time of withdrawal.

Source: Ministry of Health

That being said, financing 100% of long-term care needs through personal assets may not be the most efficient option compared to risk pooling mechanisms such as CareShield Life and personal insurance. The key reason is that risk pooling provides greater financial resources than relying solely on personal assets.

Havend’s Planning Methodology

At Havend, we believe in making insurance solutions more realistic, reasonable, and cost-effective through our time-tested framework. By using this framework, we offer a better understanding of how individuals can evaluate and make decisions about their needs and the amount required during severe disability events.

Source: By Havend 2024

Conclusion

Understanding the level of caregiving you may need and preparing for the associated costs in the event of severe disability is crucial. This is especially vital for pre-retirees who have not yet addressed this in their planning. The costs can be significant and ignoring them could jeopardise their financial security. With life expectancies rising, planning for a potential lifespan of 100 years is no longer optional – it is essential.

Don’t leave your future to chance. By taking proactive steps now, you can ensure that you and your loved ones are protected from the financial strain and emotional burden of long-term care. Assess your current care needs, explore the available financial options, and secure a comprehensive plan that aligns with your goals and circumstances.

At Havend, we are dedicated to helping you navigate these challenges with confidence. Reach out to us for a personalised consultation and take the first step toward securing your financial and emotional well-being. For a complimentary InsureWell Assessment from one of our Insurance Specialists, contact us at contact@havend.com. Your future self will thank you for the decisions you make today!

This is an original article written by our Insurance Specialist at Havend.

At Havend, if we are found to have oversold you, we have put in place a Money Back Guarantee (MBG) scheme, so you can trust that we will always prioritise your interests first. Unprecedented in Singapore, learn more about our Money Back Guarantee scheme here.